The NGS Market Is Not Out of the Woods. But the Odds Are Starting to Look Better.

Los Angeles, December 9th, 2025

The last few years have not been easy for the NGS tools market. After the COVID-era distortion, the industry had to work through a difficult hangover: cautious academic budgets, tighter biopharma spending, China weakness, instrument-cycle uncertainty, and continued pricing pressure. In other words, the market had to pay for its sins. Some of those sins were committed by customers, some by vendors, and a few by my Excel models.

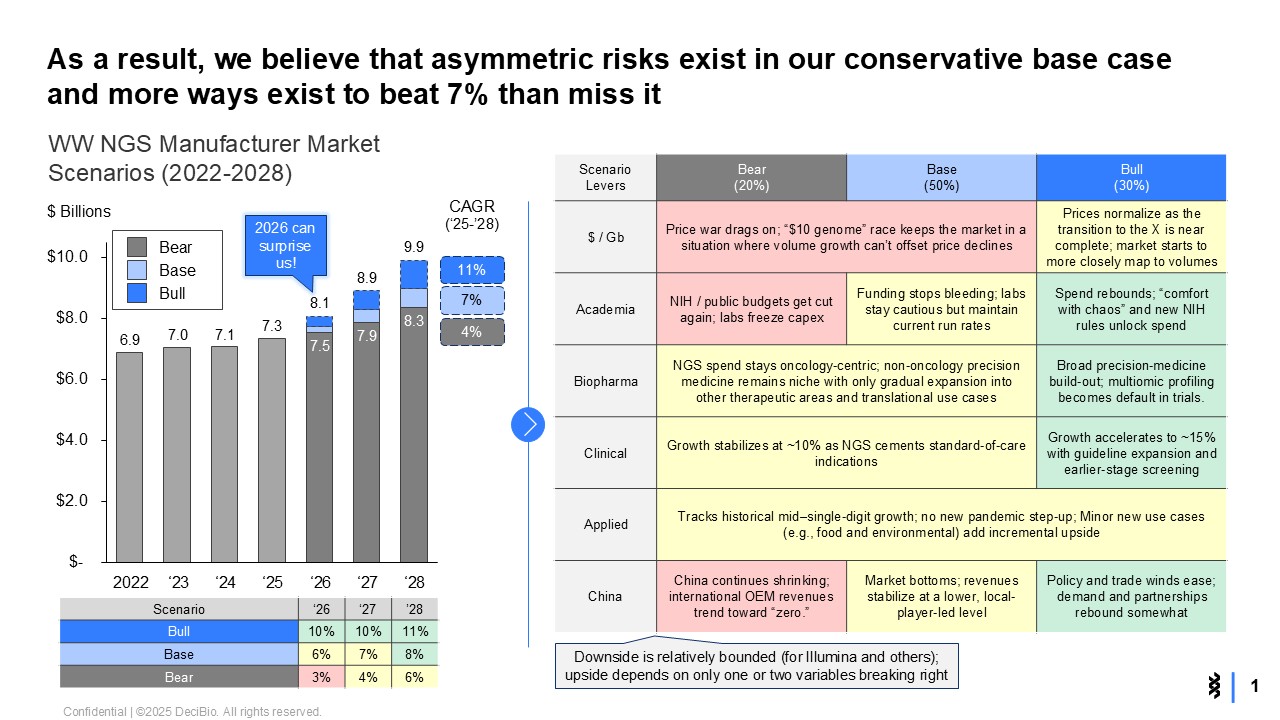

But the key takeaway from our latest NGS manufacturer market scenarios is that the downside now looks relatively bounded, while the upside has multiple ways to surprise.

In our conservative base case, we see the worldwide NGS manufacturer market growing at ~7% p.a. from 2025 to 2028, reaching ~$8.9B by 2028. That base case assumes the market does not snap back dramatically. It assumes pricing pressure continues, academic funding remains cautious, biopharma growth is steady but not euphoric, clinical growth stabilizes around core standard-of-care indications, and China only begins to bottom.

That is hardly a heroic forecast. But given my recent track record, it is intentionally sober. And yet, even from that conservative base, we believe the risk is asymmetric: there are more ways for the market to beat 7% than to miss it.

The downside is real — but increasingly concentrated

The bear case is not hard to imagine. Price per Gb continues to decline faster than volume can compensate. NIH and public budgets remain pressured. China continues to shrink as international OEM revenue trends toward zero. Biopharma remains oncology-centric, with only gradual expansion into other therapeutic areas.

In that scenario, the market still grows, but only ~4% p.a., reaching about $8.3B by 2028. That is not exciting. But it is also not catastrophic.

The reason is simple: NGS has moved from "interesting research technology" to embedded infrastructure across large parts of translational research, oncology, rare disease, reproductive health, infectious disease surveillance, and biopharma development. Once technology becomes infrastructure, customers may delay, negotiate, or sweat assets longer — but they rarely go backward.

Sequencing may still be cyclical, but it is no longer optional.

The base case is deliberately conservative

Our base case assumes no major inflection in academic funding, no dramatic China rebound, no sudden reacceleration in applied markets, and no overnight decentralization of clinical NGS. It also assumes that price normalization takes time and that vendors continue to compete hard on cost per Gb.

Under that scenario, growth is driven by the slow but steady expansion of core clinical indications, continued biopharma demand, and incremental adoption in translational workflows.

This is the "no champagne, no panic" scenario. The market keeps growing because NGS is increasingly tied to decisions that matter: which therapy to use, which patient to enroll, which recurrence to catch, which rare disease to diagnose, and which biology to understand before someone spends $200M moving a drug forward.

The bull case does not require everything to go right

And finally, the most interesting part of the analysis is the bull case.

We estimate an upside scenario of growth at ~11% p.a., with the market approaching $10B by 2028. Importantly, this does not require every lever to break perfectly. It requires one or two major variables to improve.

A few examples:

- Academic spending could rebound as funding uncertainty clears and labs regain confidence.

- Biopharma could broaden beyond oncology into multiomic profiling across immunology, neurology, inflammation, and other therapeutic areas.

- Clinical growth could accelerate as guidelines expand, reimbursement improves, and earlier-stage screening and monitoring use cases move closer to routine adoption.

- China could stabilize at a lower base and begin to contribute again, even modestly.

- Pricing could normalize as the transition to newer platforms matures and vendors shift from pure price-per-Gb competition toward workflow, data quality, sample-to-answer value, and clinical utility.

None of these is guaranteed. But none is science fiction either.

The market is shifting from "more sequencing" to "better use of sequencing"

The biggest strategic point is that the next phase of NGS growth will not simply be about generating more bases at lower cost. That story still matters, of course. Cost curves have powered this industry for two decades. But the next layer of value will come from how sequencing is embedded into workflows, evidence generation, clinical decisions, and multiomic interpretation. That is why the market can grow even if the hardware cycle remains choppy. The value is moving from the box to the system around the box.

What this means for NGS manufacturers

For NGS manufacturers, the message is clear: the market is not going back to the easy-growth days. Customers are more disciplined. Capital is more selective. Procurement is more sophisticated. And everyone has learned to ask whether the shiny new instrument actually solves a workflow problem or just looks good in a launch video.

But this is still one of the most important technology markets in life sciences. Alien technology.

The next phase will reward companies that can do three things well:

- First, defend the core by delivering reliable, cost-effective sequencing at scale.

- Second, expand the use cases by making NGS easier to adopt in clinical, biopharma, and applied settings.

- Third, capture more of the workflow by connecting instruments, chemistries, informatics, interpretation, and evidence into a more complete solution.

Just execution.

Bottom line

Our view is that the NGS manufacturer market has entered a more mature, more scrutinized, but still highly attractive phase.

The bear case is no longer a collapse story. The base case is solid but conservative. The bull case has several plausible paths. After several years of digestion, the NGS market may finally be moving from "when does the hangover end?" to "what does the next growth curve look like?" And this time, the answer may be less about who can sequence the cheapest — and more about who can make sequencing indispensable.